Property TDS Payment

When buying a property worth ₹50 lakh or more in India, the buyer must deduct 1% Property TDS Payment from the total amount and pay it to the government under Section 194-IA of the Income Tax Act. The buyer needs to fill Form 26QB online, make the Property TDS Payment through net banking or at an authorized bank, and then download Form 16B as a TDS certificate to give to the seller. This Property TDS Payment must be made within 30 days of the transaction, and both the buyer’s and seller’s PAN details are required. Failure to pay TDS on time may lead to penalties. The seller receives the payment after TDS deduction, and the buyer must ensure compliance to avoid legal issues.

Professional Property TDS?

TDS on Property – Section 194IA of Income Tax Act, 1961

Section 194IA of the Income Tax Act, 1961, requires the buyer to deduct TDS when purchasing immovable property (excluding agricultural land) if the sale consideration is ₹50 lakh or more. The applicable TDS rate is 1% of the total sale amount, and if the seller does not provide a PAN, the rate increases to 20%. The deduction must be made at the time of payment to the seller, and the buyer must deposit the TDS with the government using Form 26QB within 30 days from the end of the month in which the deduction is made. After depositing the TDS, the buyer is responsible for issuing Form 16B (TDS certificate) to the seller as proof of deduction.

The buyer holds full responsibility for deducting and depositing the TDS, and any failure to do so may result in penalties. If there are multiple buyers or sellers, the TDS is deducted in proportion to their respective ownership shares. Unlike other tax provisions, TDS under Section 194IA is calculated based on the actual sale consideration and not the stamp duty value. This provision ensures tax compliance in high-value property transactions and helps track real estate transactions more effectively.

Benefits of Property TDS Payment

Legal Compliance

Ensures you follow tax laws and avoid penalties from the Income Tax Department.

Avoid Penalties & Interest

Late or non-payment can result in fines and interest charges.

Proof of Payment

Serves as proof that tax has been deducted and deposited with the government.

Eases Tax Filing for Seller

The seller can claim credit for the TDS paid while filing their tax return.

Transparency in Property Transactions

Helps in tracking large property transactions and curbing tax evasion.

Reduces Future Tax Liability

Ensures the seller’s tax is partly paid in advance, reducing tax burden later.

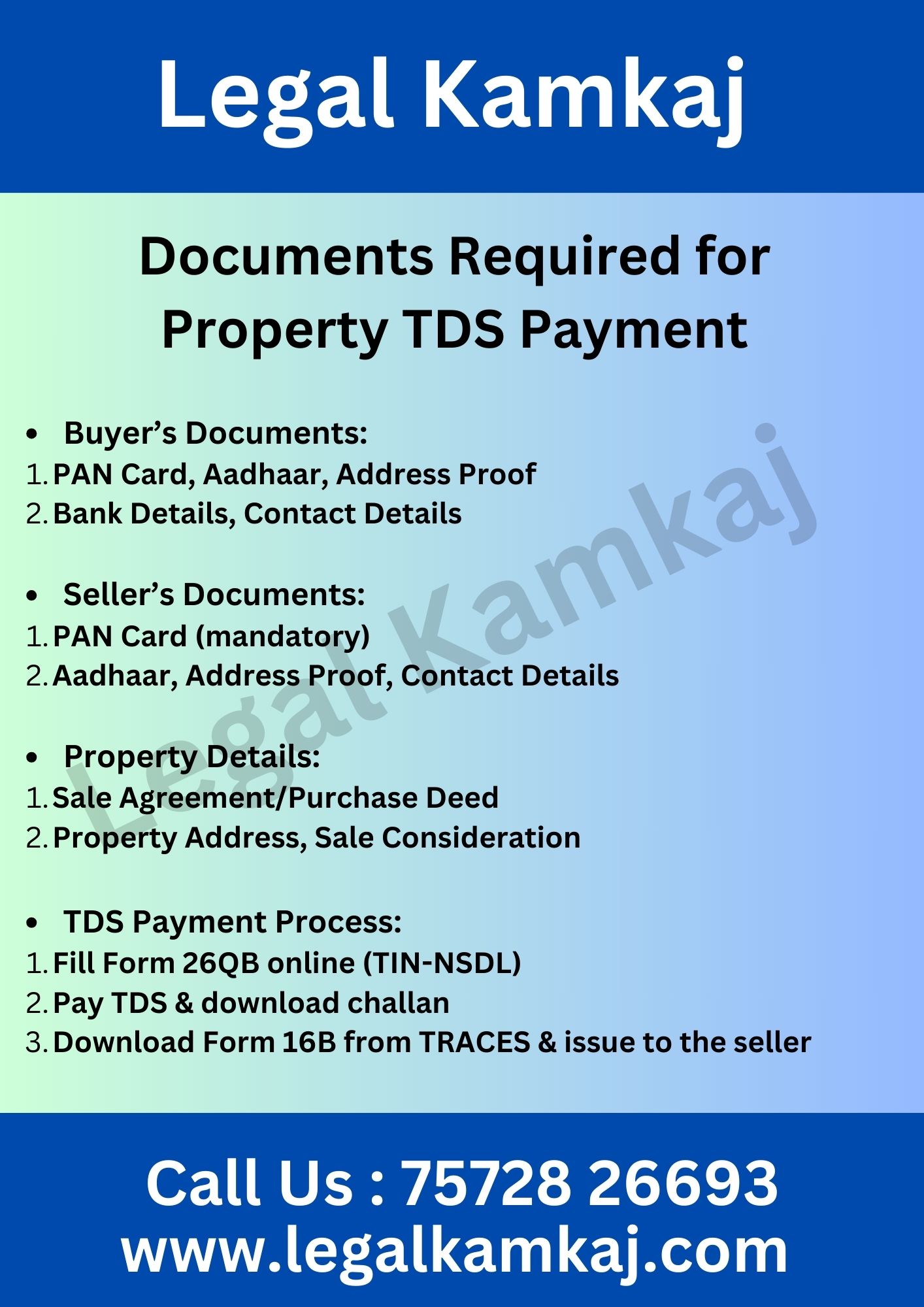

Documents Required for Property TDS Payment

- Buyer’s Documents:

- PAN Card, Aadhaar, Address Proof

- Bank Details, Contact Details

- Seller’s Documents:

- PAN Card (mandatory)

- Aadhaar, Address Proof, Contact Details

- Property Details:

- Sale Agreement/Purchase Deed

- Property Address, Sale Consideration

- TDS Payment Process:

- Fill Form 26QB online (TIN-NSDL)

- Pay TDS & download challan

- Download Form 16B from TRACES & issue to the seller

Property TDS Payment Forms & Charges

Here’s a detailed breakdown of TDS on Property (Under Section 194IA, 194IB & 194IC) along with applicable forms and charges:

TDS Type

Applicable Form

Rate

Professional Fee

TDS on Property Purchase

(if property value > ₹50 Lakh)

Form 26QB

1% of Property Value

Rs. 2,000 Per Return

TDS on Rent (if rent > ₹50,000 per month)

Form 26QC

5% of Annual Rent

Rs. 1,500 Per Return

TDS on Joint Development Agreement (Landowner’s Share of Consideration)

Form 26QD

10% of Consideration

Rs. 3,000 Per Return

Additional Charges (If Applicable):

- Late Payment Interest: 1% – 1.5% per month

- Late Filing Penalty: Rs .200 per day (max Rs. 10,000)

- Correction in TDS Returns: Rs. 1,500

- TDS Notice Handling & Compliance Support: Rs. 2,000

How to File TDS on Property (Form 26QB)?

- Visit TIN-NSDL

- Select Form 26QB (TDS on Property)

- Fill Details (Buyer & Seller PAN, Property & Payment Info)

- Pay TDS (1% of Sale Value) & Download Challan 280

- Download Form 16B from TRACES after 5-7 days & give it to the seller

Understanding TDS on Property Sales for NRI Vendors

- TDS Rate for NRI Property Sales

- When an NRI sells property in India, the buyer must deduct TDS at a rate of 40% on capital gains. If the property is held for less than two years, the gains are considered short-term and taxed at 30%. Conversely, for long-term capital gains (properties held for over two years), the TDS rate drops to 20% on indexed capital gains.

- When an NRI sells property in India, the buyer must deduct TDS at a rate of 40% on capital gains. If the property is held for less than two years, the gains are considered short-term and taxed at 30%. Conversely, for long-term capital gains (properties held for over two years), the TDS rate drops to 20% on indexed capital gains.

- Calculation of Capital Gains

- To calculate short-term capital gains (STCG), use the formula: Sale Price – Purchase Price. For long-term capital gains (LTCG), apply the formula: Sale Price – Indexed Cost of Acquisition. The indexed cost adjusts the purchase price for inflation using the Cost Inflation Index (CII).

- To calculate short-term capital gains (STCG), use the formula: Sale Price – Purchase Price. For long-term capital gains (LTCG), apply the formula: Sale Price – Indexed Cost of Acquisition. The indexed cost adjusts the purchase price for inflation using the Cost Inflation Index (CII).

- Filing and Payment

- The buyer is responsible for deducting TDS and depositing it with the government using Form 26QB. The buyer must deposit the TDS amount within 30 days from the end of the month in which the tax is deducted. Afterward, the buyer must provide a TDS certificate (Form 16B) to the seller as proof of payment.

- The buyer is responsible for deducting TDS and depositing it with the government using Form 26QB. The buyer must deposit the TDS amount within 30 days from the end of the month in which the tax is deducted. Afterward, the buyer must provide a TDS certificate (Form 16B) to the seller as proof of payment.

- Exemption from TDS

- If the NRI vendor qualifies for exemptions under sections like 54, 54EC, or 54F, they can claim these exemptions by submitting the necessary documents to the buyer.

- If the NRI vendor qualifies for exemptions under sections like 54, 54EC, or 54F, they can claim these exemptions by submitting the necessary documents to the buyer.

- PAN Requirement

- NRIs must obtain a Permanent Account Number (PAN) for TDS compliance. The buyer needs this PAN to deduct and deposit TDS accurately.

- NRIs must obtain a Permanent Account Number (PAN) for TDS compliance. The buyer needs this PAN to deduct and deposit TDS accurately.

- Double Taxation Avoidance Agreement (DTAA)

- If the NRI resides in a country with a DTAA with India, they may qualify for a lower TDS rate by providing a Tax Residency Certificate (TRC) to the buyer.

- If the NRI resides in a country with a DTAA with India, they may qualify for a lower TDS rate by providing a Tax Residency Certificate (TRC) to the buyer.

- Refund of Excess TDS

- If TDS is deducted at a higher rate or on a larger amount, the NRI can file for a refund by submitting a tax return in India.

Step-by-Step Guide to Form 16 for Property TDS

Step 1: Understanding TDS on Property Sale

- TDS applies when a property sells for more than ₹50 lakh. The rate stands at 1% of the total sale consideration if the seller is an individual or HUF (Hindu Undivided Family). The buyer is responsible for deducting and depositing TDS with the government.

- TDS applies when a property sells for more than ₹50 lakh. The rate stands at 1% of the total sale consideration if the seller is an individual or HUF (Hindu Undivided Family). The buyer is responsible for deducting and depositing TDS with the government.

Step 2: TDS Deduction Process

- Calculate the total sale consideration and determine the TDS (1% of the sale price). Next, fill out Form 26QB, available on the Income Tax Department’s website, and pay the TDS online through the NSDL e-payment facility.

- Calculate the total sale consideration and determine the TDS (1% of the sale price). Next, fill out Form 26QB, available on the Income Tax Department’s website, and pay the TDS online through the NSDL e-payment facility.

Step 3: Obtaining Form 16A

- After depositing the TDS, the buyer should obtain Form 16A as a TDS certificate. Download Form 16A from the TRACES portal after 10-15 days of TDS payment.

- After depositing the TDS, the buyer should obtain Form 16A as a TDS certificate. Download Form 16A from the TRACES portal after 10-15 days of TDS payment.

Step 4: Preparing Form 16

- Prepare Form 16, which acts as a consolidated TDS certificate issued by the buyer to the seller, including details like TDS amount, PAN of the seller, and transaction specifics.

- Prepare Form 16, which acts as a consolidated TDS certificate issued by the buyer to the seller, including details like TDS amount, PAN of the seller, and transaction specifics.

Step 5: Issuing Form 16 to Seller

- Provide Form 16 to the seller as proof of TDS deduction. The seller should verify that all details are accurate.

- Provide Form 16 to the seller as proof of TDS deduction. The seller should verify that all details are accurate.

Step 6: Seller’s Responsibilities

- Include the deducted TDS in the Income Tax Return (ITR) under capital gains and claim credit for the TDS amount.

Frequently Asked Questions

TDS on property serves as an important tax obligation that buyers must fulfill when purchasing property valued at ₹50 lakh or more. Specifically, the buyer must deduct 1% of the total sale amount. Moreover, this deducted amount must then be paid to the government. Thus, buyers need to ensure timely compliance to avoid penalties. Furthermore, accurate documentation is essential throughout this process. In addition, buyers should complete Form 26QB to facilitate this payment. Consequently, understanding these requirements not only helps in ensuring compliance but also smoothens the transaction. Ultimately, fulfilling this obligation reflects the buyer’s commitment to adhering to tax regulations, thereby contributing to the overall legal framework surrounding property transactions.

The buyer of the property is responsible for deducting TDS before making the payment to the seller and then remitting it to the government.

The TDS rate on property transactions is generally 1% of the sale consideration for residential properties and 2% for non-residential properties.